It’s the shale (aka. tight) oil, stupid. Despite all reports to the contrary, the unconventional oil boom implies rising output outside of OPEC, and OPEC will produce much less than previously expected.

Fatih Birol, IEA's Chief Economist announced the new Outlook. Picture: Shale world blog

Fatih Birol, IEA's Chief Economist announced the new Outlook. Picture: Shale world blog

The International Energy Agency (IEA) published its annual “World Energy Outlook” report last week. This caused quite a stir in the media, with many sources claiming that the IEA had changed last year’s “optimistic” (US shale oil brings a revolution) take to a more “pessimistic” one: if Middle Eastern countries postpone their investments because of the unconventional oil boom, their hesitation may result in a supply-side squeeze in oil markets. In other words, prices could be high, because sufficient oil supply would be delayed.

Sure, this is catchy; but it’s not what the IEA’s forecast numbers reflect.

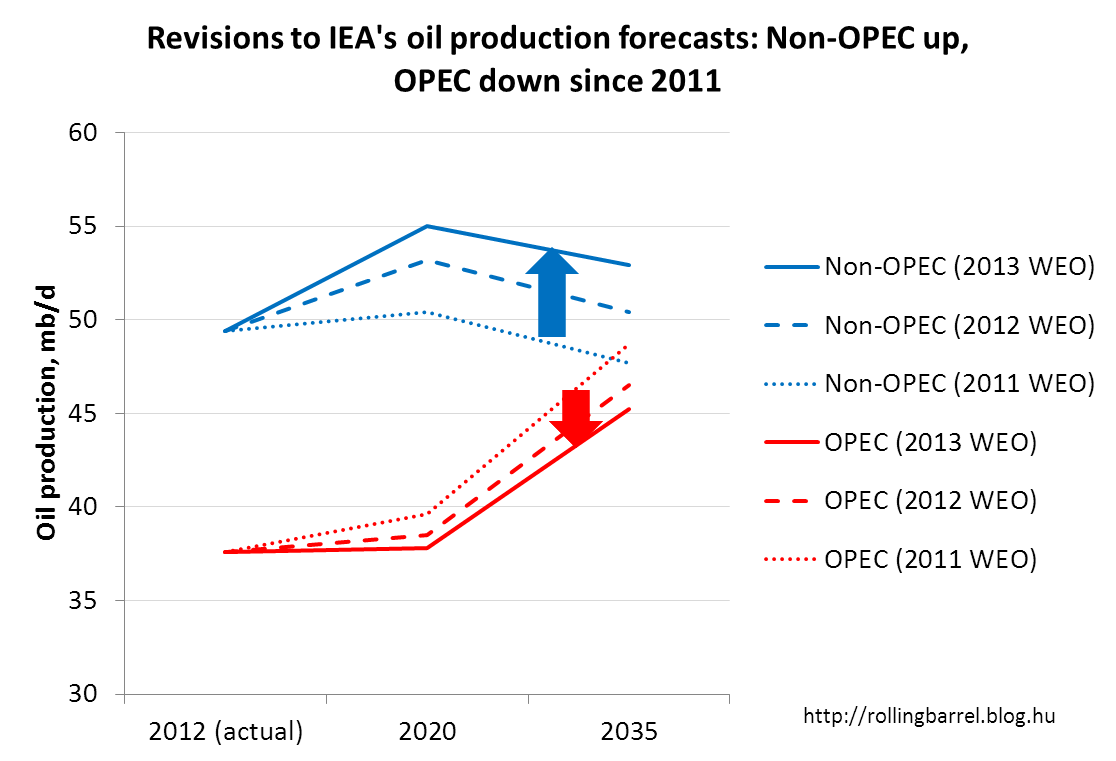

The chart below compares the IEA’s most recent oil production forecasts with its predictions published the year before and in 2011. Two years ago (as the dotted line shows), they believed only OPEC countries could substantially increase their output over the coming decades, while non-OPEC production would pretty much stagnate until 2020, and then decline.

The recent revisions tell the story. Data: IEA World Energy Outlook 2011, 2012 and 2013

The recent revisions tell the story. Data: IEA World Energy Outlook 2011, 2012 and 2013

But then came the shale oil (or, more specifically, tight oil) boom: today, the IEA’s experts think (as the continuous lines indicate) that following in the US’s footsteps, oil output in non-OPEC countries could rise significantly until 2020. Non-OPEC sources would produce around 10% more than supposed in the 2011 outlook. This implies that OPEC output is likely to stagnate until 2020, despite growing energy demand from China and other emerging economies.

The graphic below also shows that the IEA is simultaneously raising its oil demand forecast: this is particularly apparent in 2020, when the changes in OPEC’s production forecast are much smaller than in the case of non-OPEC countries.

The IEA thinks the story might change again from around 2020: tight oil production stalls, so non-OPEC production starts to decline. This gap is filled by an increase in OPEC’s output, as they still have vast and relatively low-cost reserves. So the old story (OPEC members’ growing role) still holds true according to the IEA, but is delayed by at least 10 years…

The chart above makes clear that if last year’s Outlook was labeled “optimistic” then the current one is even more optimistic (global oil production is higher and OPEC’s power declines).

For the OPEC members of course this is rather bad news: if I were an OPEC-producer, I would also take a “wait and see” approach and not be investing heavily. No one really knows what comes after 2020; we could still see some new twists and turns in the story. Which, by the way, has so far seemed to closely follow the storyline of shale gas, with analysts revising forecasts higher and higher again. (This is not that surprising given a brand new and evolving technology.) Moreover, as we recently wrote, Iran’s potential coming back from the cold could also narrow the playing field for the other OPEC members (and so could Iraq boosting its production).

A lesson is that the more catchy the title of a news story, the more suspicious it is. (One of our favorite recent examples: there is no global wine shortage, even if the media said there was.)

Another lesson is that when dealing with such long-term forecasts, because of the inherent uncertainty surrounding them, it probably makes more sense to check when and how much the forecasts change (and what the “front” of the forecast looks like), rather than what they say would be the exact figures in 25 years’ time.

So what does the IEA say about oil prices? That they will continue to increase. They have barely touched their price forecasts compared to those in 2011. Is this consistent with the story above? And what are the other key statements of the World Energy Outlook? We will get back to these questions in another post...

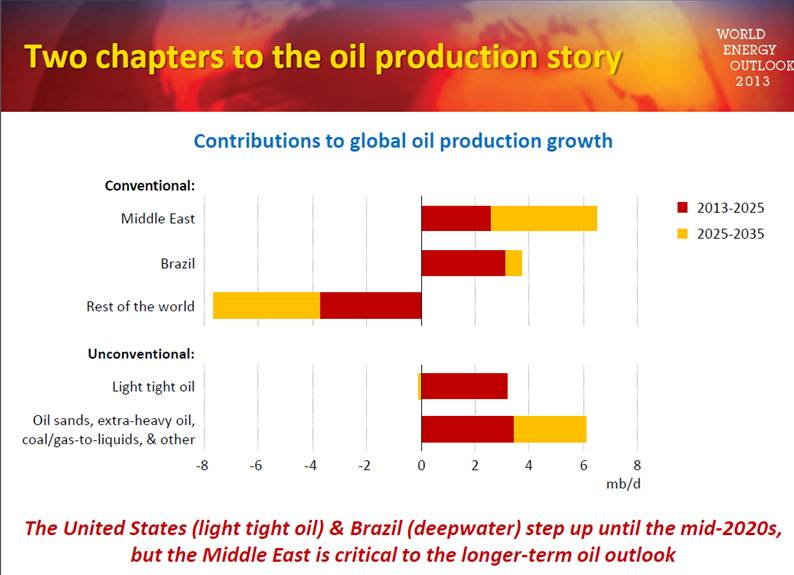

Two chapters to the oil production story, from IEA's World Energy Outlook chartpack:

Ajánlott bejegyzések:

A bejegyzés trackback címe:

Kommentek:

A hozzászólások a vonatkozó jogszabályok értelmében felhasználói tartalomnak minősülnek, értük a szolgáltatás technikai üzemeltetője semmilyen felelősséget nem vállal, azokat nem ellenőrzi. Kifogás esetén forduljon a blog szerkesztőjéhez. Részletek a Felhasználási feltételekben és az adatvédelmi tájékoztatóban.